Payers should participate in both upside and downside risk models.

Use of health IT is vital to managing and analyzing supporting data.

How we pay for health care is undergoing a disruptive, fundamental shift. We are rapidly moving away from the traditional fee-for-service, pay-for-volume approach to value-based care (VBC) programs that pay based upon demonstrated value. According to the Health Care Payment Learning & Action Network (LAN), nearly 36% of total American health care payments were tied to alternative payment models in 2018, specifically shared risk/shared savings categories.

These efforts have been successful with payers reducing unnecessary medical costs by nearly 6% as a result of their value-based care strategies. While progress has been made, there still are opportunities for payers and providers to make their transition to value-based care even more successful. Here are several things that will pave the on-ramp to VBC.

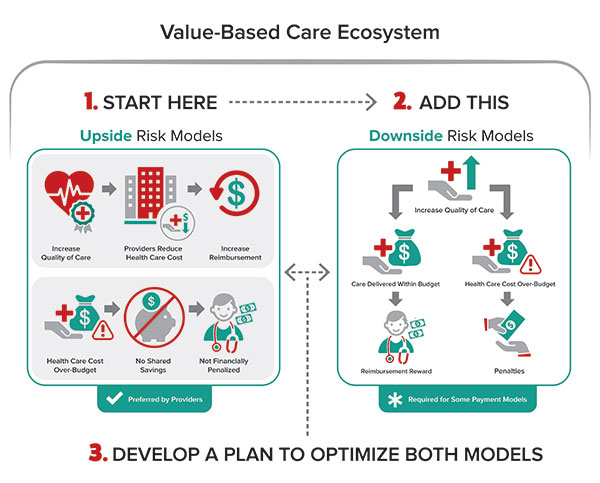

1. Embrace upside risk. Tectonic shifts in the market are moving it toward new models of financial risk sharing as the backbone of VBC models. These are aimed at making providers more accountable and financially responsible for the care they provide. One-sided or “upside risk” models allow providers to share in the savings they generate when they provide more efficient care based on certain cost, care delivery and quality metrics. In the second model, called “downside risk” arrangements, providers’ payments can get dinged when they go beyond contractually set financial and clinical levels. In fact, they may even be required to refund a portion of their payments if they go over an agreed-upon amount for a certain group of services. There are even hybrid models that can include both types of risk sharing.

Payers and providers will have a hard time ignoring these risk models going forward. By 2025, LAN projects 100% of Medicare and 50% of Medicaid and commercial payments will be tied to two-sided risk alternative payment models or APMs (categories 3B, 4A, 4B, & 4C of the LAN’s Refreshed APM Framework). By starting with upside risk and maturing to downside risk, payers will be able to increase care quality, reduce costs and increase reimbursement. Here are a few reasons why.

There are benefits. Payers save money. Providers can earn bonuses and are not liable to repay financial losses if care costs go over budget.

The train has left the station. The number of payers and providers participating in upside-only risk contracting is on the rise. This is fueled by a specialized risk-contracting method called accountable care organizations (ACOs). According to one estimate, in early 2018 there were 1,477 ACOs among public and private payers, covering about 32.7 million patients. Of those, nearly half were Medicare ACOs, the majority of which were participating in upside-only contracts. Medicare Advantage (MA) plans also are a factor. There were more than 3,000 MA plans in 2019 with an enrollment of 22 million (about a third of all Medicare beneficiaries). Medicare is the big dog on the block and Medicaid and private insurers generally follow suit.

There are risks for nonparticipation. To be sure, there are many markets where shared savings arrangements are not dominant. However, that is changing and there are consequences for payers and providers who don’t join in. Remaining independent providers that aren’t onboard risk sustainability, may join networks of other independent providers, become boutique providers or get absorbed in a merger or acquisition. Market forces and Medicare are driving commercial payers into risk-sharing arrangements. These new contracts are being written that will both create and cement trust relationships as well as establish partnerships that speak to future viability. Those who are late adopters or laggards are apt to struggle for market share and achieve competitive advantage farther down the line.

There’s already a transition to downside risk. Payers are already starting to move from upside risk arrangements to embrace downside risk arrangements. Leading the pack is Medicare’s “Pathways to Success,” which went live on January 1, 2020. There will be two payment tracks. ACOs in the BASIC track will be required to accept modest downside risk after two years, but this eventually will increase over time. ACOs in the ENHANCED track are eligible to share 75% of the savings they earn but also face downside risk of 40% to 75% of losses if their actual spending exceeds their annual benchmark. For 2018, Medicare paid approximately $285 million as shared savings to ACOs and recouped nearly $64 million as shared losses.

Leverage health information technology to manage and analyze data. Risk-based arrangements depend on data. There’s plenty of data about patients, costs, care delivery and quality, and the volume is growing using disparate clinical and administrative databases. That said, there are challenges in capturing and analyzing the data as well as sharing the information among payers, providers, patients and their caregivers.

Providers and payers are key to the required data. Payers provide a broader view from pharmacy benefits and claims, while providers have information about individual patients, costs and quality metrics through their electronic health records (EHRs). The technical challenges are exacerbated when dealing with various patient populations. At the same time, organizations will need health information technology (health IT) to help make their organizations more consumer centric, recognizing that consumer satisfaction and loyalty are critical to success in a value-based care environment.

Here are some of the ways payers and providers can leverage health IT in the world of VBC.

SELF-ASSESSMENT QUESTIONS:

Do you understand the landscape?

Where is your organization now?

Do you have a roadmap for advancing your value-based care strategy?

Move to APIs. Payers and providers will need to embrace the move to share data through application program interfaces (APIs). This is already happening with heavy impetus from the federal government. Examples include requirements in implementing the 21st Century Cures Act and the new five-year roadmap from the Office of the National Coordinator for Healthcare Information Technology. It emphasizes use of apps and APIs to help patients and providers access and share patient data. Medicare launched its Blue Button 2.0, which is a developer-friendly, standards-based API that enables Medicare beneficiaries to connect their claims data to various applications, services and research programs. In addition, fee-for-service Medicare has funded significant API standards development around payer-to-provider collaboration through Health Level 7’s (HL7) Da Vinci Project. Mobile health (mhealth) also represents a real opportunity since nearly everybody has a smart phone. Innovative mobile applications are flooding the market. It is estimated there are now over 318,000 health apps available on the top app stores worldwide — roughly twice the number available in 2015. More than 200 apps hit the market each day. Moreover, there is at least one high-quality app for each step of the patient journey. Such mhealth apps show promise for better doctor-patient communication and enhanced data management, as well as improved patient monitoring and engagement in their care. For example, use of digital health apps has been shown to reduce acute care utilization in five key patient groups (diabetes prevention, diabetes, asthma, cardiac rehabilitation and pulmonary rehabilitation). This could save health care an estimated $7 billion per year.

Embrace data analytics. Data analytics will be vital to understanding the costs and outcomes of care. For payers, this will take the form of artificial intelligence (AI). AI’s computing power can make sense of large, complex data streams. The result: actionable information for decision making. For example, risk-sharing models analyze prescribing patterns to manage high-cost patients. Providers will use the analytics in their EHRs to evaluate cost and quality performance in real time.

Standardize rules about data sharing among trading partners. Data sharing also is important to VBC but is challenged by variations in technologies and standards. This will be mitigated, to some extent, by the upcoming final rule being developed for the Trusted Exchange Framework and Common Agreement (TEFCA). Its goal is to provide a standardized, secure and scalable data exchange framework that will serve as a “single on-ramp.” Yet the individual stakeholders must internalize those requirements. Moreover, it will take a while to get TEFCA implemented. In the meantime, stakeholders must deal with trading partners whose health IT systems have different capabilities and are undergirded by different versions of standards — or even different standards. Everyone must be on the same page and trading partners need to standardize data-sharing rules among them. There’s no sense reinventing the wheel with each trading partner agreement.

Develop a compliance roadmap. As the industry forges ahead with a paradigm shift to value-based care, stakeholders need a multi-faceted approach to ensure compliance with evolving standards and mandates and to take judicious advantage of industry pilots.

Get involved with cross-industry collaborations concerning standards or stay informed at a minimum. Payers and providers should participate in new stakeholder initiatives concerning standards. It may not seem revolutionary, but it is a way to make sure your voice is heard, and your concerns are addressed. It also is a way to develop subject-matter expertise. There are several collaborations from which to choose — and they are growing. For example, several leading payers, providers, vendors and standards groups are driving to advance electronic prior authorization (ePA). America’s Health Insurance Plans (AHIP), a major insurance industry group, and several member insurers (covering 60 million lives) recently launched a pilot program based on the ePA standard. HL7’s Da Vinci Project is working to advance the use of the Fast Healthcare Interoperability Resource standard in support of VBC data exchange across communities. Da Vinci’s open business model process enables payers, health systems and other industry participants to identify and enumerate use cases that involve managing and sharing clinical and administrative data between industry partners. That said, most industry standards development organizations and collaboratives depend on paid staff and volunteers — either on their own time or on loan from their day jobs. The latter may not be practical for some organizations. To be sure, there is a broader world beyond the collaboratives that smart organizations need to keep on top of. This is an essential part of the compliance roadmap (referenced previously) and a necessity in creating strategic positioning, return on investment and compliance. •

Next Steps to VBC Success VBC and health IT are complex, rapidly growing and inextricably intertwined. Point-of-Care Partners (POCP) is a major player. We are actively involved in the development and adoption of standards for pharmacy, health data exchange and price transparency. We are the program management office for Da Vinci. Let us put our expertise to work for you. We can be your trusted partner and resource, keeping you current on trends and developments and helping you build and execute a roadmap for success and compliance. Reach out to us at gary.austin@pocp.com or jocelyn.keegan@pocp.com.

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful.

Strictly Necessary Cookies

Strictly Necessary Cookie should be enabled at all times so that we can save your preferences for cookie settings.

If you disable this cookie, we will not be able to save your preferences. This means that every time you visit this website you will need to enable or disable cookies again.

")